(The following commentary is a summary of discussions among members of the Breckinridge Capital Advisors Investment Committee (IC) as they reviewed monthly activity in the markets and investment returns. All data is as of May 31, 2026, unless otherwise noted. The members of the Investment Committee, under the leadership of Co-Chief Investment Officers Matthew Buscone and Jeffrey Glenn, CFA, are Co-Heads of Research, Nicholas Elfner and Adam Stern, J.D., M.P.A.; and Portfolio Manager and Director, Corporate Research, Josh Perez, CFA.)

Market Review

Economic data released during May continued to point to a resilient U.S. economy, despite elevated interest rates and the rise in the price of oil. Strength in artificial intelligence (AI)-related capital expenditures continued to support corporate earnings growth and equity market performance, while spending by higher-income consumers remained sufficient to offset ongoing pressure among lower-income households. Consumer savings rates declined further and delinquencies on credit cards, student loans, and auto loans remained elevated, highlighting the uneven nature of economic activity.

Inflation remained a central focus for markets. Although headline and core personal consumption expenditures (PCE) readings came in slightly below expectations, broader underlying inflation measures continued to deteriorate. Core PCE remained elevated at 3.3 percent year-over-year, and the Federal Reserve's (Fed’s) policy stance became increasingly hawkish, as inflation pressures showed limited signs of easing.

Treasury yields moved modestly higher during the month. The 10-year Treasury yield rose 7 basis points (bps), while the 2-year and 5-year Treasury yields increased 13bps and 14bps, respectively (See Figure 1). The 30-year Treasury yield increased 1bp.

During the month, the 10-year Treasury yield reached as high as 4.66 percent before retracing part of the move into month-end. The IC continues to expect a higher-for-longer rate environment, reflecting persistent inflation pressures, increased Treasury issuance, fiscal concerns, and rising global yields.

Bond market volatility remained relatively stable during May, after a mid-month spike. The ICE Bank of America/Merrill Lynch (MOVE) Index, a widely followed measure of Treasury market volatility, was little changed over the month after declining from elevated levels reached earlier in the spring (See Figure 2). While volatility remained below the peaks observed in March and April, it continued to hover near its trailing 200-day average of 73.51, reflecting ongoing uncertainty surrounding inflation, Federal Reserve policy, and the path of interest rates.

The IC modestly extended duration targets across most strategies during the month while maintaining an overall constructive outlook on economic growth and credit fundamentals.

The IC expects the Fed to remain on hold through year-end. While a range of interest rate outcomes remains possible, members believe risks are increasingly skewed toward higher yields over the next 12 months, supported by resilient growth, persistent inflation, and continued Treasury supply. The IC raised the high side of their forecast to 4.75 percent but kept the low end at 4 percent.

Municipal Market Review

The BBG Municipal Bond Index generated a 0.37 percent return in May, as municipal markets recovered from a mid-month selloff. During the same period, the BBG Managed Money Short/Intermediate Index returned 0.13 percent. Municipal yields increased modestly, with 2-, 5-, and 10-year yields rising 1bp, 4bps, and 2bps, respectively (See Figure 3). The 30-year yield was unchanged during the month.

Municipal/Treasury (M/T) ratios1 ended May little-changed month-over-month at 61 percent, 62 percent, 67 percent, and 87 percent across the 2-, 5-, 10-, and 30-year maturities, respectively (See Figure 4).

Market technicals remained supportive. Municipal bond issuance totaled approximately $54.9 billion in May, consistent with the elevated pace seen throughout 2026. Despite heavy issuance, fund flows remained strong, with municipal bond funds recording approximately $4.9 billion of net inflows during the month. Inflows continue at a record pace and have successfully absorbed new issue supply, which is running ahead of last year's record-setting volume.

Credit fundamentals remained stable. April state tax collections were generally strong, supported by healthy personal income and sales tax growth. Improving revenue conditions in California have mitigated fiscal year 2027-2028 budget pressures and contributed to stable pension funding expectations. Looking ahead, June seasonal reinvestment flows from maturities and coupon payments are expected to provide additional support for municipal valuations.

Corporate Market Review

The BBG U.S. IG Corporate Index total return was 0.76 percent in May, generating 0.56 percent of excess return, as credit spreads tightened. The option-adjusted spread on the Index narrowed 7bps to 72bps during the month, reflecting continued investor demand for IG credit. BBB-rated issuers outperformed A-rated issuers, as lower-quality segments of the IG market benefited from improving risk sentiment. The highest-rated segment of the market earned the strongest total returns.

Corporate issuance remained robust. Corporations issued approximately $192.3 billion of IG-rated debt during May, representing an increase of roughly 27 percent year-over-year. Investor demand remained strong, supported by approximately $83 billion of taxable bond inflows over the trailing 30-day period.

Credit fundamentals continued to benefit from strong earnings growth and ongoing investment associated with AI infrastructure and datacenter construction. Merger and acquisition activity has accelerated amid supportive financing conditions and elevated equity valuations, although debt-funded transactions have remained more limited than initially expected.

The best-performing sectors were Leisure, Wirelines, Technology, Independent Oil and Gas Producers, and Life Insurance. The worst-performing sectors were Supranationals, Sovereigns, Foreign Agencies, Foreign Local Government, and Construction Machinery.

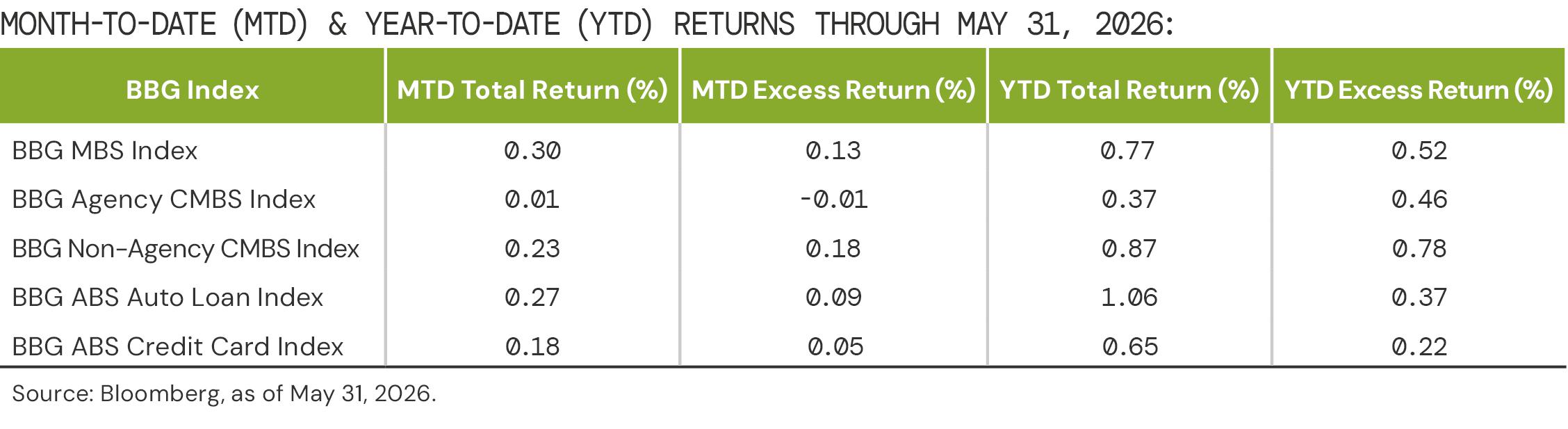

Securitized Market Review

Mortgage-related securities produced positive results during May. The BBG MBS Index returned 0.30 percent and generated 0.13 percent of excess return. Agency MBS spreads were modestly wider during the month, although the sector continued to benefit from declining rate volatility later in May. Housing market fundamentals remained subdued, as mortgage rates near 6.5 percent continued to weigh on affordability and housing demand.

Commercial mortgage-backed securities (CMBS) performance was mixed. Agency CMBS generated a 0.01 percent return and slightly negative excess returns, while non-agency CMBS outperformed, as spreads tightened. Market fundamentals remained stable and issuance activity continued to improve, supported by growth in single-asset/single-borrower transactions.

Auto loan ABS outperformed credit card ABS, as spreads tightened across consumer securitized sectors. New issue supply remained healthy, with issuance volumes running approximately 15 percent above year-ago levels. Despite increasing pressure on lower-income consumers, credit performance remained stable within higher-quality ABS sectors.

Equity Market Review

The S&P 500 gained 5.26 percent in May, extending its strong performance, as investors continued to reward companies positioned to benefit from AI-driven investment spending. The S&P 500 was up about 16 percent across April and May 2026, a two-month surge matched only four other times since 1950, according to Dow Jones Market Data.

Equity market volatility declined during May, as investor sentiment improved alongside strong earnings growth and continued enthusiasm for Information Technology-related investment themes. The Chicago Board Options Exchange (CBOE) Volatility Index (VIX) trended lower during the month (See Figure 5). Despite the decline in volatility, investors continued to monitor inflation and Fed policy expectations, as key drivers of market risk.

Growth stocks outperformed value stocks, with the Russell 1000 Growth Index advancing 7.20 percent compared with a 2.95 percent gain for the Russell 1000 Value Index.

Sector performance was led by Information Technology, which gained 15.99 percent during the month. Consumer Discretionary and Health Care also posted positive returns. Energy, Utilities, Consumer Staples, and Financials lagged the broader market. Market leadership continued to favor growth, momentum, and higher-beta factors, while dividend yield, payout ratio, and value-oriented factors underperformed.

Corporate earnings remained a key support for equity valuations. First-quarter 2026 earnings growth reached 27 percent year-over-year, representing the strongest quarterly earnings growth since the post-pandemic rebound in late 2021. Earnings growth among the Magnificent Seven2 cohort reached 63 percent, while the remainder of the S&P 500 generated approximately 17 percent earnings growth.

Equity valuations continued to rise during May, with the S&P 500 forward price-to-earnings ratio increasing to approximately 21.1 times earnings, above both its 5-year and 10-year historical averages. Despite elevated valuations, strong earnings momentum and favorable growth expectations continued to support investor sentiment.

[1] The Municipal/Treasury (M/T) ratio compares yields of municipal bonds with those of U.S. Treasury bonds of the same maturity. M/T ratios can show the relative value of municipal bonds compared with taxable bonds, by indicating when yields for municipal bonds exceed the after-tax yields on taxable bonds.

[2] Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla.

BCAI-06082026-ttqzee0v (6/9/2026)

DISCLAIMERS:

This material provides general information and should not be construed as a solicitation or offer of services or products or as legal, tax or investment advice. Nothing contained herein should be considered a guide to security selection, asset allocation or portfolio construction.

All information and opinions are current as of the dates indicated and are subject to change. Breckinridge believes the data provided by unaffiliated third parties to be reliable but investors should conduct their own independent verification prior to use. Some economic and market conditions contained herein have been obtained from published sources and/or prepared by third parties, and in certain cases have not been updated through the date hereof.

There is no assurance that any estimate, target, projection or forward-looking statement (collectively, “estimates”) included in this material will be accurate or prove to be profitable; actual results may differ substantially. Breckinridge estimates are based on Breckinridge’s research, analysis and assumptions. Other events that were not considered in formulating such projections could occur and may significantly affect the outcome, returns or performance.

Yields and other characteristics are metrics that can help investors in valuing a security, portfolio or composite. Yields do not represent performance results but they are one of several components that contribute to the return of a security, portfolio or composite. Yields and other characteristics are presented gross of advisory fees.

Index results are shown for illustrative purposes and do not represent the performance of any specific investment. Indices are unmanaged and investors cannot directly invest in them. They do not reflect any management, custody, transaction or other expenses, and generally assume reinvestment of dividends, income and capital gains. Performance of indices may be more or less volatile than any investment strategy.

Fixed income investments have varying degrees of credit risk, interest rate risk, default risk, and prepayment and extension risk. In general, bond prices rise when interest rates fall and vice versa.

Equity investments are volatile and can decline significantly in response to investor reception of the issuer, market, economic, industry, political, regulatory or other conditions.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg does not approve or endorse this material or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The S&P500 Index (“Index”) and associated data is a product of S&P Dow Jones Indices LLC, its affiliates and/or their licensors and has been licensed for use by Breckinridge. © 2026 S&P Dow Jones Indices LLC, its affiliates and/or their licensors. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC. For more information on any of S&P Dow Jones Indices LLC’s indices please visit www.spdji.com. S&P® is a registered trademark of Standard & Poor’s Financial Services LLC (“SPFS”) and Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”). Neither S&P Dow Jones Indices LLC, SPFS, Dow Jones, their affiliates nor their licensors (“S&P DJI”) make any representation or warranty, express or implied, as to the ability of any index to accurately represent the asset class or market sector that it purports to represent and S&P DJI shall have no liability for any errors, omissions, or interruptions of any index or the data included therein.

Subscribe to Insights

Sign up to receive curated insights directly in your inbox.