Premium Bonds 101

Premium bonds and the math behind them continue to furrow the brows of many municipal investors. A premium bond is one that sells at a higher price than its par value (typically $100), or principal. It is a legitimate mind-bender for investors, as it would seem counterintuitive to intentionally purchase a bond at say, $108.50, knowing that you will receive less than that ($100) at maturity.

However, it turns out that premium coupons have some potential advantages. They can be more defensive in a rising interest rate environment and potentially less volatile. Additionally, they are generally more liquid than discount municipal bonds because premiums are typically the preferred and more-prevalent coupon structure in the municipal bond market.

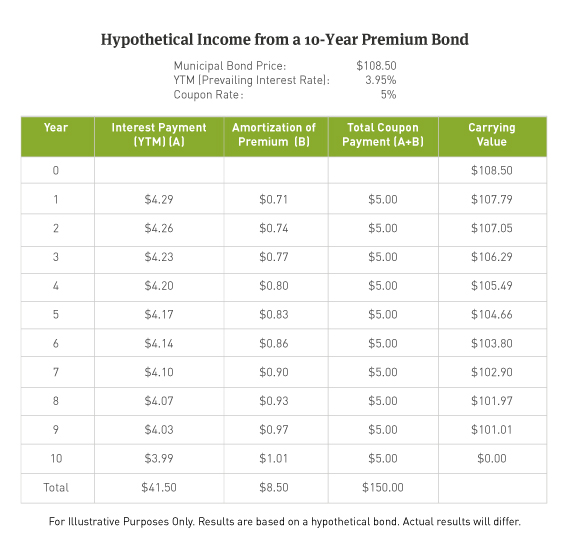

To understand these advantages, investors must first grasp an important concept: bondholders do not lose the premium paid on a premium bond. If an investor buys a bond at $108.50 that matures at $100, they would not lose that extra $8.50; instead, that amount would be returned to them over the life of the bond in the form of higher coupon payments.

Table 1 shows the mechanics of the cash flows of a premium bond. With premium bonds, the coupon rate is higher than the yield to maturity (YTM). This is because each coupon payment comprises not only the YTM (Column A), but also the return of a portion of the premium to the bondholder (Column B). (By contrast, for discount bonds the coupon rate is lower than the YTM). Premium bondholders do not experience a capital gain or loss if they hold the bond until maturity.

Knowing this, investors can be open to capitalizing on the structural advantages offered by premium bonds over par/discount bonds, which include:

POTENTIALLY LESS-TROUBLESOME TAXATION1

According to IRS rules, investors purchasing bonds at a market discount must pay ordinary income tax on some portion of the discount. In this way, discount bondholders own bonds in which a portion of the return is taxable, and a portion is tax-exempt. Discount bonds not only require a tax outlay, but in our experience, they are also more difficult for investors to understand and value.

It is important to remember that federal and local tax laws and rates can change at any time; changes to tax laws and rates can impact tax consequences for investors. Investors should consult with their tax professionals regarding tax management strategies and associated consequences.

LIQUIDITY

Due to the tax implications and complexity of discount bonds, they are generally less liquid than premium bonds. As of September 30, 2022, 5 percent coupons were the most prevalent in the municipal market, making them more liquid. On the other hand, par bonds are typically only available when a bond is first issued.

SHORTER DURATION

Discount bonds typically have lower coupons and longer durations because more of an investor’s principal is earned at maturity. Premium bonds have a shorter duration than par/discount bonds because they allow investors to build income faster, so the shorter duration offered by premium bonds can improve total return if rates go up – an important consideration as the U.S. Federal Reserve has continued its aggressive series of interest rate hikes. The higher income generated by increased coupon payments could help offset some of the price declines as rates rise. Also, with higher coupon payments, investors are able to reinvest the funds and take advantage of higher rates.

AVAILABILITY OF TAX LOSS SWAPS

Tax loss swaps can help municipal investors by offsetting large taxable gains with losses on the municipal side.2 Given the lower liquidity in municipal market, tax concerns and lower coupons of discount bonds, rate normalization could be particularly detrimental to them. If rates rise, the loss on a par/discount bond may be too large for a tax loss swap to work. This could negatively impact investors with heavy tax burdens, because it makes the swap more difficult and costly to execute.

The immediate takeaway is that discount bonds are potentially harder to sell, as sellers must offer several layers of discounts to entice investors to purchase them. The first layer is the market discount embedded in the bond itself. The second layer is the present value of the future tax liability discussed above. This is less of an issue for longer-term bonds in which this liability is spread out over longer time periods. But for intermediate-term bonds, this can make a significant difference in where the bond can be sold. The third layer is an amount to compensate investors for the lower liquidity of par/discount bonds. Premium bonds are not subject to these layers of discounting, and offer certain structural benefits in a rising rate environment.

We think premium bonds offer value in many interest rate environments. They can offer a defensive position when rates rise. Because they historically have retained their value more so than discount bonds, they have been more liquid than discount bonds.

A Word About Risks

Investors should be mindful that all investing involves risk, and that principal loss is possible. Investing in municipal bonds, regardless of whether they are discount or premium bonds, involves interest rate risk, credit risk and market risk. In addition, income from municipal bonds can be declared taxable because of unfavorable changes in tax laws, adverse interpretations by the IRS or state tax authorities, or noncompliant conduct of a bond issuer.

[1] Specifically, the IRS allows for a discount totaling 0.25 points per year based on the bond’s remaining time to maturity.

[2] In a tax loss swap, an investor will sell a bond for a loss and replace it with another bond with a similar maturity or credit profile. Due to differences in tax rates, swaps may not be appropriate for certain individuals and the results of swaps do not guarantee a profit or significant tax advantage.

DISCLAIMER

This material provides general and/or educational information and should not be construed as a solicitation or offer of Breckinridge services or products or as legal, tax or investment advice. The content is current as of the time of writing or as designated within the material. All information, including the opinions and views of Breckinridge, is subject to change without notice.

Any estimates, targets, and projections are based on Breckinridge research, analysis, and assumptions. No assurances can be made that any such estimate, target or projection will be accurate; actual results may differ substantially.

Past performance is not a guarantee of future results. Breckinridge makes no assurances, warranties or representations that any strategies described herein will meet their investment objectives or incur any profits. Any index results shown are for illustrative purposes and do not represent the performance of any specific investment. Indices are unmanaged and investors cannot directly invest in them. They do not reflect any management, custody, transaction or other expenses, and generally assume reinvestment of dividends, income and capital gains. Performance of indices may be more or less volatile than any investment strategy.

Performance results for Breckinridge’s investment strategies include the reinvestment of interest and any other earnings, but do not reflect any brokerage or trading costs a client would have paid. Results may not reflect the impact that any material market or economic factors would have had on the accounts during the time period. Due to differences in client restrictions, objectives, cash flows, and other such factors, individual client account performance may differ substantially from the performance presented.

All investments involve risk, including loss of principal. Diversification cannot assure a profit or protect against loss. Fixed income investments have varying degrees of credit risk, interest rate risk, default risk, and prepayment and extension risk. In general, bond prices rise when interest rates fall and vice versa. This effect is usually more pronounced for longer-term securities. Income from municipal bonds can be declared taxable because of unfavorable changes in tax laws, adverse interpretations by the IRS or state tax authorities, or noncompliant conduct of a bond issuer.

Breckinridge believes that the assessment of ESG risks, including those associated with climate change, can improve overall risk analysis. When integrating ESG analysis with traditional financial analysis, Breckinridge’s investment team will consider ESG factors but may conclude that other attributes outweigh the ESG considerations when making investment decisions.

There is no guarantee that integrating ESG analysis will improve risk-adjusted returns, lower portfolio volatility over any specific time period, or outperform the broader market or other strategies that do not utilize ESG analysis when selecting investments. The consideration of ESG factors may limit investment opportunities available to a portfolio. In addition, ESG data often lacks standardization, consistency and transparency and for certain companies such data may not be available, complete or accurate.

Breckinridge’s ESG analysis is based on third party data and Breckinridge analysts’ internal analysis. Analysts will review a variety of sources such as corporate sustainability reports, data subscriptions, and research reports to obtain available metrics for internally developed ESG frameworks. Qualitative ESG information is obtained from corporate sustainability reports, engagement discussion with corporate management teams, among others. A high sustainability rating does not mean it will be included in a portfolio, nor does it mean that a bond will provide profits or avoid losses.

Net Zero alignment and classifications are defined by Breckinridge and are subjective in nature. Although our classification methodology is informed by the Net Zero Investment Framework Implementation Guide as outlined by the Institutional Investors Group on Climate Change, it may not align with the methodology or definition used by other companies or advisors. Breckinridge is a member of the Partnership for Carbon Accounting Financials and uses the financed emissions methodology to track, monitor and allocate emissions. These differences should be considered when comparing Net Zero application and strategies.

Targets and goals for Net Zero can change over time and could differ from individual client portfolios. Breckinridge will continue to invest in companies with exposure to fossil fuels; however, we may adjust our exposure to these types of investments based on net zero alignment and classifications over time.

Any specific securities mentioned are for illustrative and example only. They do not necessarily represent actual investments in any client portfolio.

The effectiveness of any tax management strategy is largely dependent on each client’s entire tax and investment profile, including investments made outside of Breckinridge’s advisory services. As such, there is a risk that the strategy used to reduce the tax liability of the client is not the most effective for every client. Breckinridge is not a tax advisor and does not provide personal tax advice. Investors should consult with their tax professionals regarding tax strategies and associated consequences.

Federal and local tax laws can change at any time. These changes can impact tax consequences for investors, who should consult with a tax professional before making any decisions.

The content may contain information taken from unaffiliated third-party sources. Breckinridge believes the data provided by unaffiliated third parties to be reliable but investors should conduct their own independent verification prior to use. Some economic and market conditions contained herein have been obtained from published sources and/or prepared by third parties, and in certain cases have not been updated through the date hereof. All information contained herein is subject to revision. Any third-party websites included in the content has been provided for reference only. Please see the Terms & Conditions page for third party licensing disclaimers.